At first sight, the Victorian Ombudsman Report, ‘An Investigation into the management of complex workers compensation claims and WorkSafe oversight’ seems like a grenade dropped into the status quo of workers compensation in Australia!

The report prepared by the Ombudsman, Deborah Glass OBE clarifies however that the problems identified do not relate to the entire Victorian compensation system:

‘However my investigation did not extend to the entire WorkSafe claims management system and the evidence of this investigation does not indicate that it is broken. On the contrary, as WorkSafe points out, 80% of claims are finalised within 13 weeks of injury, and its last annual survey of injured workers recorded satisfaction of over 85%’

The conclusions reached by an organisation not primarily concerned with insurance or compensation issues that peeks into the world of workers’ compensation is however, quite instructive.

The 170 page report highlights issues in the management of claims by WorkSafe Agents, the private insurance companies that administer compensation benefits, and the oversight provided by WorkSafe Victoria. The emphasis is on the 20% of claims that are considered complex that make up 90% of the scheme’s liabilities.

Of particular interest is the focus on how financial incentives drive claims agent behaviour and the negative impact of some of those behaviours on the health and well-being of the injured workers that the scheme is supposed to serve.

The Report’s Executive Summary includes the following statements:

‘But evidence of unreasonable decision-making strongly suggests that in disputed and complex matters the financial measures are encouraging a focus on terminating and rejecting claims to achieve the financial rewards’

and

‘There is also evidence that four of the five agents manipulated, or that staff contemplated manipulating, claims in order to achieve the financial rewards or avoid penalties’

Given the focus of this blog and previous commentary on issues relating to IME assessments, the Ombudsman’s comments about WorkSafe’s oversight of the IME System is also worthwhile reading.

The report is positive about WorkSafe’s initiatives stating:

‘Worksafe has gradually improved and strengthened its management of the IME system, but there is scope for further improvement, including:

- targeting its quality assurance process to those IME’s subject to a high number of complaints

- systematically reviewing agent claims decisions where a deficient IME report is identified, to examine whether the agent incorrectly disentitled a worker

The report also makes the following suggestion:

‘Providing workers with a choice of IME and requiring the sharing of IME reports with treating health practitioners could have made a significant difference to many of the complaints to my office’

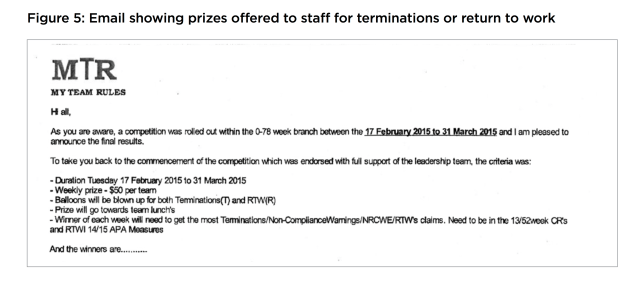

The Ombudsman had access to email trails which revealed thinking by WorkSafe Agents about use of IME opinions and choice of IME’s to achieve particular outcomes. The de-identified email below is reproduced in the report:

The Report states (P 49):

‘In some cases, the evidence suggested that agents’ choice of IME’s may have been motivated by the opportunity to obtain an opinion from an IME who was considered to hold particular views’

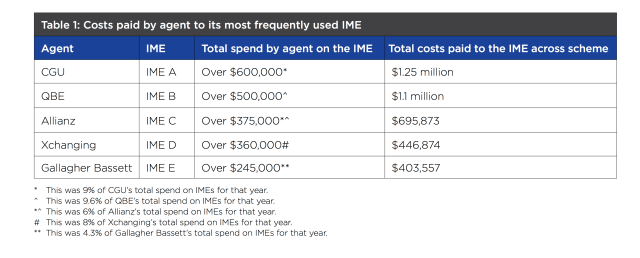

The cost data about spending on IME opinions is also of interest suggesting that interdependent relationships develop between some IME’s and WorkSafe Agents.

Highlighting these relationships is reminiscent of the expose of similar relationships between ACC in New Zealand and IME’s who operate in that system:

The Accident Compensation Conciliation Service (ACCS) also expressed concern in relation to matters that go to conciliation:

The agents rely ‘on a small pool of heavily used IME’s, many of whom are largely removed from current clinical practice’

The report highlights the financially orientated workplace culture of the WorkSafe Agents with rewards and prizes for staff who achieved the most terminations. There was evidence that Agent’s behaviour is strongly influenced by the substantial financial rewards and penalties paid by WorkSafe to the detriment of the individual claimants, their health and the stated objectives of the scheme.

The email below about prizes offered is a sad reflection of an Agent’s workplace culture:

The report includes references to information provided by professionals and industry groups. Notably the Australian Medical Association stated:

‘Suffering an injury is difficult for anyone. This hurt is often exacerbated by rejection and suspension of claims for medical and like expenses. These decisions by agents are often overturned at Medical Panels or during conciliation. Both processes lead to a delay in return to work and health. These rejections, even if subsequently rectified, can seriously damage injured workers’ recovery’

For me, the most important conclusion in the report is this:

‘WorkSafe’s oversight needs to directly target the management of complex, disputed claims to ensure that there is a safety net for the most vulnerable’

WHAT DOES IT ALL MEAN?

The issues raised in the Ombudsman’s Report are nothing new, but when highlighted by a credible organisation and its recommendations for improvements are accepted by WorkSafe Victoria, the concerns cannot be ignored.

The findings have relevance, I am sure, for all workers compensation jurisdictions and perhaps more widely for other types of insurance where an individual’s health care is involved.

The Main Stream Media have taken an interest recently in several matters relevant to management of claims related to injury and ill-health.

There was the CommInsure Scandal, where claimants of Life, Income Protection and Disability Insurance were receiving poor treatment at the hands of a major financial organisation. Then there was the article in the Conversation about use of covert surveillance by MetLife on Police Force claimants with PTSD in New South Wales and now the Victorian Ombudsman’s Report which raises issues about management of claims by yet another group of financial organisations, the WorkCover Claims Agents in Victoria – Allianz, CGU, Gallagher Bassett, QBE, and Xchanging.

It does raise the question about the logic of having financial organisations in control of people’s health, whether in the context of workers’ compensation, motor accident injury insurance or with life, income protection and disability schemes.

Can any socially just system operate satisfactorily where there are direct financial benefits to the organisation from denying or delaying treatment or where funding for treatment is contingent on savings from a reduction in income support payments? At the very least there should be transparency about the financial incentives that operate within such schemes.

TASMANIA’S SCORECARD

It is interesting to compare the issues highlighted in the Ombudsman’s report with those in Tasmania and the measures in Tasmania already in place to address those issues.

Many of the issues flagged in the Ombudsman’s Report have been raised in Tasmania by the Australian Medical Association locally.

In theory at least, WorkSafe in Tasmania could be considered to be in a better position to be the independent umpire in the arrangements to provide workers compensation coverage for workers in the state. In Victoria ultimately it is the Government that both underwrites the Scheme and acts as Regulator giving rise to potential for conflict of interest.

Tasmania’s workers compensation system is relatively under regulated compared to that in Victoria. Tasmania has an underwritten system where the private insurers not only administer claims, but also carry the liability. Potentially the financial incentives to manage claims to reduce costs is much greater than the financial incentives offered in Victoria by WorkSafe to insurers as its agent. The private insurers in Tasmania directly receive premium income from employers. Employers have greater input in claims management as a result. In the case of self-insurers and the State Service there is direct employer control of claims management.

In Tasmania there is a financial incentive by the insurers to reduce costs to both limit losses and at the same time remain competitive in the marketplace of a privately underwritten scheme. Concerns have been expressed that this competition has resulted in unrealistically low premium income to insurers to be able to fund their potential liability. The most recent WorkCover Tasmania annual report includes the following:

As self-insurers, The State Service and other major employers operate a system somewhat more akin with the Victorian System. The State Service contracts Jardine Lloyd Thompson to administer its claims, while some larger self-insurers like Woolworths utilise EML to administer their claims.

There is no publicly available information I am aware of about any financial incentives applied within the insurer organisations in Tasmania. It would be interesting to know if and how they operate in comparison to the incentives offered by WorkSafe to their agents in Victoria. I am only aware that one of the local insurers provides financial incentives to workplace rehabilitation provider organisations for RTW outcomes. Some of my medical colleagues and rehabilitation provider professional organisations have expressed concerns about the apparent lack of transparency about such financial arrangements.

On the other hand there are well-publicised legislated ‘incentives’ for injured workers to encourage desirable behaviour i.e. the step-down provisions in weekly payments to encourage return to work.

WorkSafe Tasmania is a relatively small and under-resourced organisation that has oversight of the system. It’s operations are funded by a levy on the Insurers in proportion to their market percentage. There are no incentives paid related to performance. The following is an excerpt from WorkCover Tasmania’s Annual report.

Some of the measures in place in Victoria are not in place here in Tasmania. For example, apart from accreditation of impairment assessors, there is no oversight of the IME system, although there are plans by WorkSafe to develop standards for IME assessors. There is no Quality Assurance or Audit System in place for IME assessors nor any plans to do so.

While Tasmania has a legislated system to provide for Medical Panels, these have been rarely used (although there are encouraging signs), whereas the issue in the Victorian System according to the Ombudsman’s Report is that binding Medical Panel decisions in that jurisdiction are not always followed by the WorkSafe Agents.

Tasmania however does have a legislated requirement for IME reports obtained by the insurers to be provided to the treating doctor, although there is currently some contention about whether that applies to all IME reports or only the initial report obtained from a particular specialist.

It is interesting that in Victoria ‘cherry picking’ or ‘doctor shopping’ for IME opinions is seen as inappropriate, while in Tasmania there seems to be widespread acceptance that there is nothing wrong with that approach where an insurer’s liability is at stake.

The issue of choice of IME is a vexed one. A recent LinkedIn article by Dr Doron Samuell, suggests that with choice of IME by the worker in the system, the process will eventually lead to the removal of all IME’s who provide reports favourable to the insurer.

3 Doctors, 1 Headache

He states:

‘It is axiomatic that insurers must have the opportunity to obtain their own evidence, this is fundamental to managing any claim. Claimants submit medical evidence from their treating doctor or commissioned medical reports. To defer to an approach, dictated by the politics of pleasing, will necessarily impact on the quality and reliability of the medical evidence that is available to the insurer. Poor decision-making, that is predicated on the medical evidence, either to accept a claim that has no merit, will only drive up costs and therefore premiums. When the premiums become unaffordable, will there be time to reflect on the pathway to collapse?’

While I have some sympathy for that view, surely it is not about whether reports are favourable or not to any particular party, rather are they objective, accurate and evidence-based. The challenge is to achieve that goal. A better approach than either insurer or worker choice of IME might be the regulator to choose a panel of suitable doctors with medical profession input and those doctors be randomly assigned to any particular case according to their accepted expertise.

Tasmania also has provision for provisional funding for treatment while initial disputes about liability are sorted out, but my experience is that it doesn’t always work well.

Victoria has an Accident Compensation Conciliation Service (ACCS) and support services WorkCover Assist and Union Assist in addition to its court system to resolve disputes, whereas in Tasmania there is no service that focuses on conciliation only Worker Assist and the Workers Rehabilitation and Compensation Tribunal.

***********************************************************

What the Victorian Ombudsman Report highlights is the risk inherent in the application of financial incentives reinforcing a financial system culture that has little or no concern for individuals or their health.

At the very least, any financial incentives should be publicly available, in the same way that the incentives to promote recovery and return to work for workers are publicised. Any incentives should be based on overall outcomes, not related to measures at an individual claim level.

The other ‘Take-Home’ message is that the focus needs to be on improving the management of the 10 or 20% of complex claims that incur the vast majority of any scheme’s liability.

WorkSafe in Victoria clearly has some work to do to rebalance priorities with the complex claims.

***********************************************************

It would be interesting if a similar independent review were conducted in the Tasmanian jurisdiction – I suspect similar issues would be identified with complex claims

COMPETITION PRINCIPLES

COMPETITION PRINCIPLES